Over 170 public companies now hold Bitcoin as a treasury asset, collectively controlling 5.5% of supply. This guide covers the complete framework: acquisition strategies, custody solutions, FASB fair value accounting (effective 2025), SEC disclosure requirements, and on-chain verification.

The Corporate Bitcoin Treasury Revolution

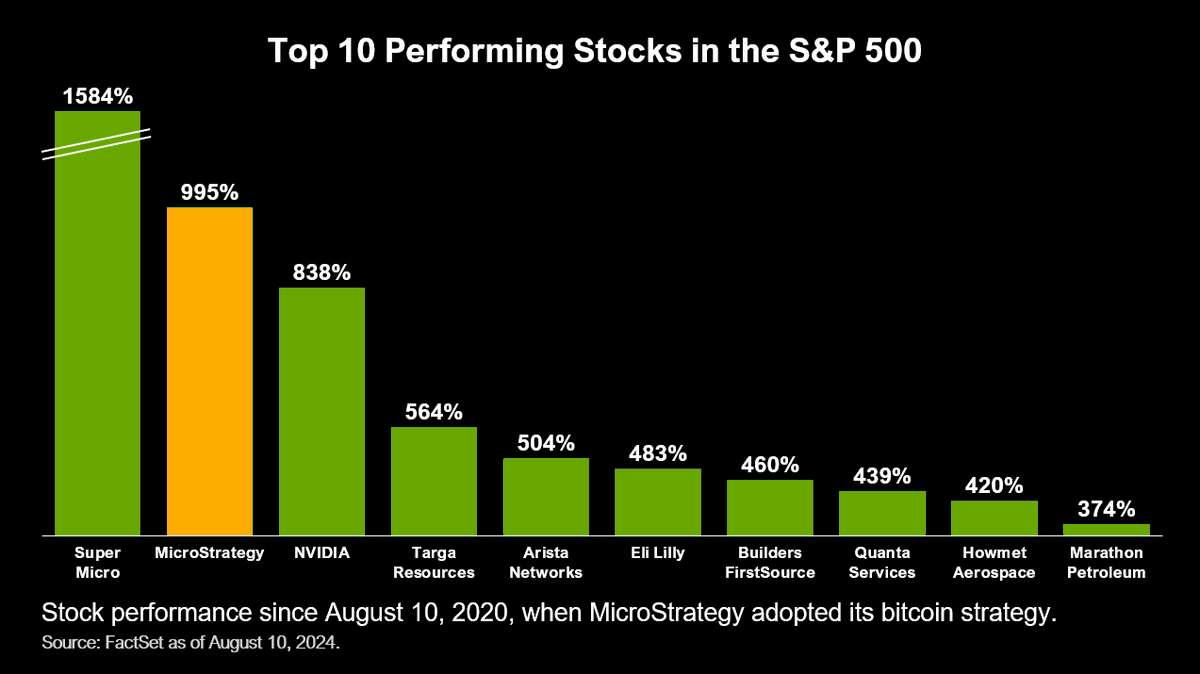

In August 2020, MicroStrategy made a bet that seemed radical at the time: convert $250 million of corporate cash into Bitcoin. Four years later, the company—now rebranded as Strategy—holds over 660,000 BTC worth $70+ billion and has outperformed 499 of 500 S&P 500 stocks.

What started as one company’s contrarian move has become a corporate movement. As of late 2025, over 170 publicly traded companies hold Bitcoin as a treasury asset, collectively controlling approximately 1.1 million BTC—about 5.5% of all Bitcoin in circulation.

Source: Bitcoin Treasuries, Yahoo Finance

Why Now?

The acceleration in 2025 isn’t coincidental. Several forces converged:

| Catalyst | Impact |

|---|---|

| FASB ASU 2023-08 | Fair value accounting effective Jan 2025—companies can now report gains, not just impairments |

| Bitcoin ETF Approval | Institutional legitimacy and easier board conversations |

| Dollar Devaluation | M2 money supply expansion forces corporations to seek hard assets |

| Proof of Concept | Strategy’s 5-year track record provides corporate blueprint |

Part 1: The Strategic Case for Bitcoin Treasury

The Problem with Cash

Michael Saylor’s framing at Bitcoin for Corporations 2025 was blunt: 96% of public companies are “zombie companies” unable to outperform a Treasury bill.

If you’re not Apple, Google, or Nvidia, you need to find a strategy to break free from the stranglehold of digital monopolies.

Michael Saylor, Bitcoin for Corporations 2025 Keynote

Source: Nasdaq

Cash sitting in a corporate treasury loses purchasing power to inflation. Even at 5% interest rates, real returns after inflation and taxes are often negative.

Bitcoin as “Digital Property”

The bull case for corporate Bitcoin holdings rests on several pillars:

- Scarcity: 21 million cap vs. unlimited fiat printing

- Portability: No counterparty risk, 24/7 liquidity

- Durability: No maintenance costs, no depreciation

- Divisibility: Can allocate any percentage of treasury

Unlike real estate or gold, Bitcoin can be acquired in any amount, verified instantly, and stored without ongoing costs.

Part 2: Acquisition Strategies

Companies use different methods to acquire Bitcoin depending on their size, risk tolerance, and capital structure.

Method 1: Cash Conversion

The simplest approach—convert existing cash reserves to Bitcoin.

Best for: Companies with excess cash, low debt, and long time horizons

Example: In 2020, MicroStrategy converted $500 million in cash generating 0% interest into Bitcoin. The company concluded Bitcoin was the best investment due to its commodity status and appreciation potential.

Source: CoinPaprika

For detailed guidance on execution: Where to Buy Bitcoin for Business

Method 2: Debt Financing

Issue bonds or convertible notes to fund Bitcoin purchases.

Best for: Companies with strong credit, access to capital markets

Example: Metaplanet issues 0% interest bonds in Japan, leveraging the yen carry trade to acquire Bitcoin essentially for free.

Read more: Metaplanet’s Yen Carry Trade Strategy

Method 3: Equity Raises

Issue new shares to fund Bitcoin acquisition.

Best for: Companies with high stock valuations relative to book value

Example: Strategy uses “at-the-market” (ATM) equity offerings, raising billions through incremental share sales to fund Bitcoin purchases.

Method 4: Revenue Allocation

Allocate a percentage of ongoing revenue to Bitcoin purchases.

Best for: Small and medium businesses starting their Bitcoin treasury

Read more: Bitcoin Treasury Strategy for Small Companies

Part 3: Custody Solutions

How you store Bitcoin is as important as how you acquire it. Corporate custody has matured significantly.

The 2025 Custody Landscape

| Custodian | Key Features |

|---|---|

| Coinbase Prime | 8 of top 10 public BTC holders use it; 81% of US ETF assets |

| Fidelity Digital Assets | Strategy moved $5.1B to Fidelity; regulated since 2018 |

| BitGo | Multi-signature, $250M insurance |

| Anchorage Digital | Federally chartered crypto bank |

Source: Decrypt, Arkham Intelligence

Custody Models

Third-Party Custody (92.4% of businesses) - Professional security, insurance, regulatory compliance - Trade-off: Counterparty risk

Self-Custody (7.6% of businesses) - Full control via multisig wallets - Trade-off: Operational complexity, key management burden

Hybrid Model (Most common in 2025) - Split holdings between custodian and self-custody - Best of both: operational efficiency + sovereignty for reserve portion

For a deep dive: Corporate Bitcoin Custody Solutions Comparison

Part 4: Accounting and Financial Reporting

The accounting treatment of Bitcoin changed dramatically in 2025.

FASB ASU 2023-08: The Game Changer

Before 2025, Bitcoin was classified as an indefinite-lived intangible asset under US GAAP. Companies could only record impairments (write-downs) but never write-ups—even if Bitcoin’s price recovered or exceeded purchase price.

This created absurd situations where profitable Bitcoin positions showed as losses on financial statements.

What Changed (Effective January 1, 2025):

| Aspect | Old Rules | ASU 2023-08 |

|---|---|---|

| Measurement | Cost minus impairment | Fair value each period |

| Gains | Only on sale | Recognized in net income |

| Balance Sheet | Buried in intangibles | Separate line item |

| Disclosure | Minimal | Detailed holdings required |

For detailed implementation guidance: Bitcoin Treasury Accounting: FASB 2025

Tax Implications

The IRS treats Bitcoin as property, meaning every sale triggers a taxable event. Recent guidance clarified that companies are not subject to the Corporate Alternate Minimum Tax (CAMT) on unrealized Bitcoin gains.

For small business considerations: Bitcoin Accounting for Small Business

Part 5: SEC Disclosure Requirements

Public companies holding Bitcoin face specific disclosure obligations.

Required Risk Factor Disclosures

The SEC expects companies to disclose material factors including:

- Price volatility: Bitcoin has traded between $26,000 and $70,000+ within 12-month periods

- Custody risks: Theft of private keys, hacking, counterparty failure

- Regulatory risks: Evolving legal landscape across jurisdictions

- Accounting volatility: Fair value changes now flow through income statement

Source: SEC.gov

What the SEC Looks For

Companies should consider making the disclosures recommended by the guidance in future filings, as the SEC staff may look to this guidance when reviewing filings from these companies.

SEC Division of Corporation Finance, April 2025

Source: Fenwick

Part 6: Verification and Transparency

How do stakeholders verify a company’s Bitcoin claims? This is where proof of reserves becomes critical.

The Verification Stack

| Method | Trust Level | Description |

|---|---|---|

| SEC Filings | Medium | Quarterly reports, but lagging and unverified |

| Attestation Reports | Medium-High | Third-party auditor confirms holdings at point in time |

| On-Chain Verification | Highest | Real-time xpub monitoring, cryptographic proof |

On-Chain Verification: The Gold Standard

Companies that publish their extended public keys (xpubs) enable real-time, cryptographic verification of holdings. No trust required—anyone can independently verify the balance.

For technical deep dive: Is It Safe to Share Your xpub?

For verification methods: How to Verify Company Bitcoin Holdings On-Chain

Proof of Reserves for Treasury Companies

Traditional proof-of-reserves (PoR) was designed for exchanges. For treasury companies, the model is simpler: they hold Bitcoin, not customer deposits.

| Approach | Best For |

|---|---|

| xpub Disclosure | Maximum transparency, real-time verification |

| Merkle Tree Proofs | Exchanges with customer liabilities |

| Third-Party Attestation | Regulatory compliance, traditional stakeholders |

Read more: Bitcoin Treasury Companies: Proof of Reserves

Part 7: Risks and Risk Management

Warning: Bitcoin treasury strategies carry significant risks. Every company considering this approach must understand and disclose these risks to stakeholders.

Price Volatility

Bitcoin can lose 50%+ of its value in months. For treasury companies:

- Liquidation risk: If holdings are collateral for debt, forced sales may occur at unfavorable prices

- Balance sheet volatility: FASB fair value accounting means Bitcoin swings flow directly to net income

- Stock correlation: Company stock often trades as leveraged Bitcoin exposure

Read more: MicroStrategy’s Time Bomb: Understanding the Bitcoin Risk

Operational Risks

- Custody failure: Exchange hacks, custodian bankruptcy

- Key management: Self-custody requires robust security practices

- Regulatory change: Unfavorable legislation could impact holdings

Concentration Risk

Many treasury companies rely on single financing sources or strategies. Diversification across custodians, funding sources, and jurisdictions reduces single points of failure.

Part 8: Case Studies

Strategy (MicroStrategy): The Pioneer

- Holdings: 660,624+ BTC ($70B+)

- Strategy: Aggressive debt and equity raises

- Result: Outperformed 499/500 S&P stocks since 2020

Metaplanet: The Yen Carry Trade

- Holdings: 35,102 BTC ($3.78B)

- Strategy: 0% interest bonds leveraging Japan’s low rates

- Result: Stock up 5,753% in 2024

Read the full analysis: Metaplanet’s Yen Carry Trade Strategy

Comparison

Read the detailed comparison: MicroStrategy vs Metaplanet: Bitcoin Strategy Compared

Getting Started: A Framework for CFOs

Step 1: Board Education

Before any allocation decision, the board needs to understand: - What Bitcoin is and isn’t - The strategic rationale - Risk factors and mitigation strategies - Accounting and disclosure implications

Step 2: Policy Development

Create a formal Bitcoin treasury policy covering: - Allocation limits (% of treasury) - Acquisition methodology - Custody requirements - Reporting frequency - Risk management procedures

Step 3: Infrastructure Setup

- Select custodian(s) with appropriate insurance and regulatory status

- Establish accounting procedures aligned with FASB ASU 2023-08

- Implement reporting dashboards for real-time visibility

Step 4: Pilot Allocation

Start small. Many companies begin with 1-5% of treasury as a pilot before committing to larger allocations.

For small business implementation: Why Every Small Business Should Consider a Bitcoin Treasury

Step 5: Verification and Transparency

Consider publishing xpub addresses for stakeholder verification. This differentiates your company as a transparent, verifiable Bitcoin holder.

Tools and methods: Best Proof of Reserve Auditors and Tools

Key Sources

Statistics and Data

- Bitcoin Treasuries - Comprehensive tracking of public company holdings

- CoinGecko Bitcoin Treasuries - Holdings data for institutions

- The Block Treasury Tracker - Corporate holdings dashboard

Accounting Standards

- FASB ASU 2023-08 - Official accounting standard

- Deloitte Implementation FAQ - Practical guidance

SEC Guidance

- SEC Division of Corporation Finance - Crypto Offerings - Disclosure requirements

- SEC Crypto ETP Guidance - Risk factor expectations

Corporate Examples

- Strategy.com - MicroStrategy’s Bitcoin strategy hub

- Metaplanet Official - Asia’s largest public Bitcoin holder

Built BitcoinCompanies so my kids can learn Bitcoin on a map full of 🐉 🐋 🐳 🦈 🐬 🐙 🐠 🦀 🦐.

Turns out adults like it too.